The contribution margin measures how efficiently a company can produce products and maintain low levels of variable costs. It is considered a managerial ratio because companies rarely report margins to the public. Instead, management uses this calculation to help improve internal procedures in the production process. For that, you’ll need a tool that automates data collection, accurately calculates financial insights, and produces customizable reports. Request a free demo and see how Cube can help you save time with all your contribution margin income statements, reports, analysis, and planning.

4: The Contribution Margin Income Statement

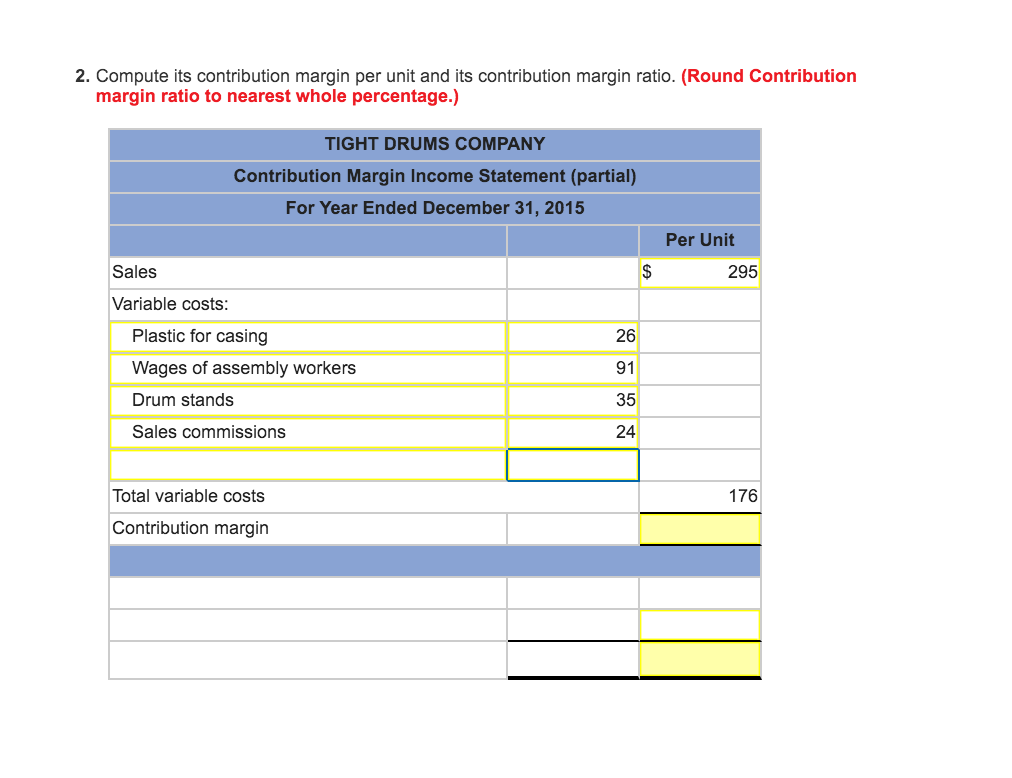

The contribution margin ratio is calculated as (Revenue – Variable Costs) / Revenue. Very low or negative contribution margin values indicate economically nonviable products whose manufacturing and sales eat up a large portion of the revenues. Alternatively, the company can also try finding ways to improve revenues.

Contribution income statement vs. traditional income statements

Sometimes a direct cost would remain even if the costobject were eliminated, but this is the exception rather than therule. To calculate the contribution margin, you need more detailed financial data to calculate EBIT. Because this figure is usually expressed as a percentage, we’d then divide the contribution margin by the revenue to get the ratio of 0.44. Quickly surface insights, drive strategic decisions, and help the business stay on track. Variable costs tend to represent expenses such as materials, shipping, and marketing, Companies can reduce these costs by identifying alternatives, such as using cheaper materials or alternative shipping providers.

Importance of Contribution Income Statements

- Fixed expenses are then subtracted to arrive at the net profit or loss for the period.

- A contribution income statement is an income statement that separates the variable expenses and fixed costs of running a business.

- Companies are not required to present such statements to any external party, so there is no need to follow GAAP or IAS.

- Instead, management needs to keep a certain minimum staffing in the production area, which does not vary for lower production volumes.

- A university van will hold eight passengers, at a cost of \(\$200\) per van.

Contribution format statements separate expenses into fixed and variable costs. Traditional income statements separate costs by production (COGS) and administration (SG&A), each of which may be a mix of variable and fixed costs. The variable costs (raw materials, packaging, commissions) total $50,000, leaving a contribution margin of $50,000. After covering fixed expenses (rent, salaries), the net profit is $25,000. This detailed breakdown helps in understanding the financial performance of individual products or services.

Example 1 – single product:

When comparing the two statements, take note of what changed and what remained the same from April to May. If the contribution margin for an ink pen is higher than that of a ball pen, the former will be given production preference owing to its higher profitability potential. Such decision-making is common to companies that manufacture a diversified portfolio of products, and management must allocate available resources in the most efficient manner to products with the highest profit potential. Where C is the contribution margin, R is the total revenue, and V represents variable costs. The following examples explain the difference between traditional income statement and variable costing income statement.

What is the Contribution Margin Income Statement?

Variable costs (or expenses) are any costs that do not remain consistent. These could include energy, wages (for labor related to production) or any other cost that raise or lower with the output levels of your business. ABC Cabinets can also use contribution margin analysis to understand each product segment’s break-even point, or the point where it begins to make a profit.

From contribution margin figure all fixed expenses are subtracted to obtain net operating income. The following simple formats of two income statements can better explain this difference. The contribution margin income statement is a superior form of presentation, because the contribution margin clearly shows the amount available to cover fixed costs and generate a profit (or loss).

(This process is the same as the one we discussed earlier for production costs.) Susan then established the cost equations shown in Table 5.5. The marketing department with the cooperation of research and development department has proposed the production of a new product. entering invoices and receipts side by side in xero Because of limited resources, the new product can only be manufactured if one of the existing products is dropped. In a different example than the previous one, if you sold 650 units in a period, resulting in $650,000 net profit, your revenue per unit is $1,000.

In the last 10 years, she has worked with clients all over the country and now sees her diagnosis as an opportunity that opened doors to a fulfilling life. Kristin is also the creator of Accounting In Focus, a website for students taking accounting courses. Since 2014, she has helped over one million students succeed in their accounting classes. More than 488 units results in a profit, and 486 units or less result in a loss.

Variable costs are less than COGS, which also may include fixed and variable costs, so a business’s contribution margin is usually higher than its gross margin. It is primarily used for external financial reporting, providing a comprehensive overview of a company’s financial performance. A contribution margin income statement is a document that tallies all of a company’s products and varying contribution margins together, helping leaders understand whether the company is profitable. It’s a useful tool for making decisions on pricing, production, and anything else that could improve profitability. However, ink pen production will be impossible without the manufacturing machine which comes at a fixed cost of $10,000.

Based on the contribution margin formula, there are two ways for a company to increase its contribution margins; They can find ways to increase revenues, or they can reduce their variable costs. A key characteristic of the contribution margin is that it remains fixed on a per unit basis irrespective of the number of units manufactured or sold. On the other hand, the net profit per unit may increase/decrease non-linearly with the number of units sold as it includes the fixed costs. The contribution margin is computed as the selling price per unit, minus the variable cost per unit. Also known as dollar contribution per unit, the measure indicates how a particular product contributes to the overall profit of the company.